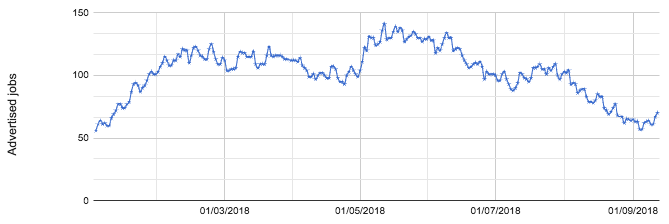

As we draw to the end of an incredible summer when British tourism must have had one of its best years in living memory, how has it been for the architecture industry? The months of July and August are traditionally very difficult to gain an accurate picture of what is happening in construction, as decision making gets delayed until everyone is back from holiday. This year has felt much longer than usual though and one summer holiday appears to be no longer enough! In terms of recruitment, however, the number of job adverts has been gradually declining since May and is now at a level not seen since January.

There have also been a few more redundancies from some of the larger studios who have had sizeable projects put on hold. Although these figures are disappointing, a number of our clients are still winning a lot of new work and feeling optimistic about the year ahead. Last week also appeared to be a turning point and the graph started heading upwards again.

The recent 10 year anniversary of the financial crisis is a good opportunity to reflect and although the jobs market is far from perfect, the industry is in a dramatically better position than it was in 2008. The architectural jobs market actually crashed about 6 months earlier than the financial markets and acts as a good bellwether for future trends. Thankfully although there is still nervousness, the situation feels a lot more positive moving towards 2019.

With fears over Brexit still looming large, however, more roles appear to be on contract until there is an increase in confidence in what is going to happen post March 29th 2019. The one impact of the referendum result that we noted last year and is starting to bear out in official figures, is the decrease in EU Architects looking to work in the UK. For people making plans for their future and where to bring up families, the Brexit situation gives no confidence to such important decisions and opportunities in mainland Europe and sometimes further afield are often more appealing.

For firms who are recruiting, feedback is often that it is getting harder to find suitably qualified Architects and especially those with strong Revit skills. Our research shows that Revit is now being requested in around 50% of job adverts. In terms of sectors, the super high-end London residential is very much struggling but larger housing, the Private Rented Sector and student housing is pretty busy, especially around the outskirts of the city. Infrastructure and transport has been quite active for the last couple of years and although Crossrail is nearing completion (albeit a little delayed), work on HS2 and a number of international transport schemes being designed by UK practices should start to take over resources.

The two other fairly positive areas of construction are the hotel and commercial sectors, where we are seeing good demand for architects.

The news during the summer, however, seemed to be a daily update on the woes of the retail industry. Hopefully though this could become an opportunity for architecture. In order to survive, the traditional high street and retail stores will need to become higher quality, mixed use spaces that make shopping more of a leisure experience. With a big shift in shopping habits online, the internet retailers are also in a race to find and build more warehouses. According to Property agent JLL, more than 12 million square feet of logistics properties, typically used for storage and distribution, were let in the first six months of the year. The take-up figure was 38% higher than a year earlier and a 90% jump on the prior six months.

With this rapidly changing environment and turbulent political scene, 9B is currently conducting an in-depth salary survey to compare with our 2016 and 2017 results. If you would like to receive a copy of the report, please complete our confidential survey and we will email you a copy.

Although recent reports have shown salaries have moved little since the last recession, hopefully the results of this year's survey will show a more positive industry.